The £91,000 Yamada Manor — Vanishing Premiums in a Forgotten Silk Insurance Chamber

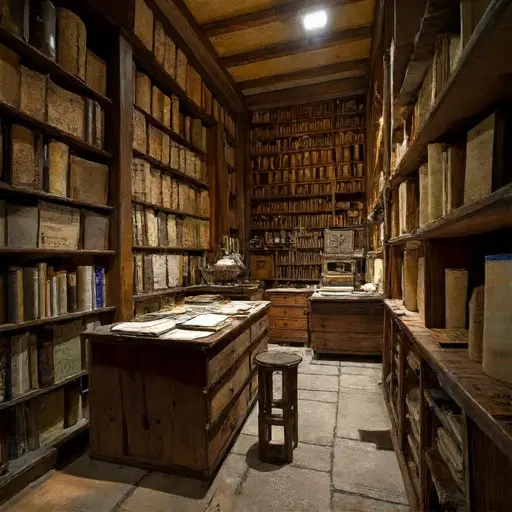

The word premiums appears repeatedly across the insurance scrolls laid out in careful rows along the central desk, each document recording coverage for silk shipments, merchant warehouses, and textile caravans. Early entries are precise, with carefully calculated risk tiers and stamped approvals, but later scrolls deteriorate into uncertainty—adjustments rewritten, coverage delayed, and entire policies marked “pending verification of transport stability.”

Haruto Seiichi Yamada, Silk Insurance Underwriter

His identity is preserved on stamped policy seals: Haruto Seiichi Yamada, Insurance Underwriter for Silk Trade.

Born 1853 in Kyoto, his profession reflects structured risk assessment tied to textile commerce routes and merchant guild agreements. A folded registry note references his wife, “Aiko Yamada,” and a daughter assisting in ledger transcription.

Seven traces define him: a brush pen frozen mid-stroke over a risk assessment sheet; a ledger marked “unverified caravan exposure index”; a drawer of policy seals unused and slightly warped; correspondence from merchant houses requesting deferred coverage decisions; a broken abacus bead set used for premium calculation; a stack of silk inspection reports never finalized; and a recurring marginal phrase—premium adjustment pending seasonal humidity confirmation.

His work depends on stable environmental conditions that gradually became unreliable across trade routes.

Breakdown of Environmental Risk Calculations

The decline begins when seasonal humidity patterns become unpredictable across silk-producing regions. Moisture damage increases during transport, invalidating previously stable risk assumptions. Yamada’s insurance tables attempt to compensate for shifting conditions, but each revision introduces further instability in premium calculations.

No fraud or cancellation is recorded. Instead, environmental unpredictability overtakes statistical modeling, leaving policies continuously reassessed but never finalized. Coverage exists in principle, but not in enforceable certainty.

In the final ledger, the focus keyword premiums appears repeatedly beside recalculated figures that never settle into a final insured value.

No policy is finalized. No risk model is confirmed. The manor remains furnished, its insurance chamber intact but inactive.

The Yamada Manor stands as a silent archive of protection calculated but never fully secured, where value exists only in perpetual reassessment.